Julia's Blog

Julia's Blog

Home Deposits – Made Simple

Two Years @ $200 Per Week and No LMI

Combine the First Home Guarantee with the Super Saver Scheme to buy a home with nearly one third of your deposit being tax savings. If you have a child the government will provide you with mortgage insurance at no cost, so you won’t need the full 20% deposit.

The ideal candidate for this arrangement is someone who is on a good income so the tax incentives are greater and they can afford the repayments on 95% of the purchase price but are struggling to get a deposit together, possibly because of high rents in the area or recent difficulties that have passed.

While this blog assumes the saver has not ever owned a house before some of these concessions such as the government guarantee for sole parents can apply to subsequent purchases of a home. And individuals can utilise the super saver scheme even if their partner has previously owned a home.

The First Home Owners Super Saver Scheme

This allows you to withdraw some of your superannuation to buy your first home but you need to make voluntary contributions first. The gift is, these contributions can come from before tax dollars. If you play your cards right it means you are only taxed at a rate of 15% on your earnings that you put aside for your home deposit.

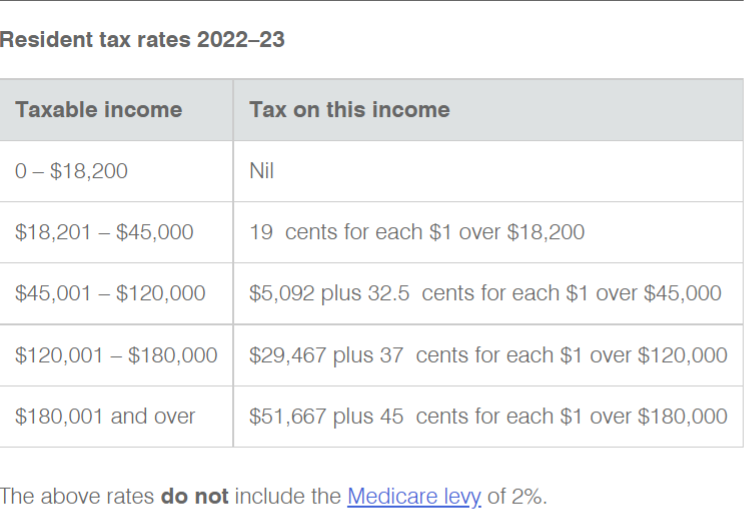

Say for example you decide you can afford to save $200 per week from your take home pay. Here are the 2022-2023 tax rates:

If you earn $140,000 a year your marginal tax rate is 39% that means for every $10,000 you earn you only get to take home $6,100. If instead, you put the money into super where it is only taxed at 15% you will have $8,500 tucked away in super, saving for your deposit. Now at $140,000 your employer will be putting $14,000 into super for you, under the guarantee. In total you can only have $27,500 in tax effective (concessional) contributions a year. To stay under the cap of $27,500 you could put an additional $13,500 into super to save for your home. If you have been on similar or lower wages over the past couple of years but not made any extra superannuation contributions then you will have over $20,000 in unused cap, this can be carried forward for up to 5 years allowing you to contribute more than $27,500. Under this super saving plan you are allowed to contribute $15,000 a year, after the 15% tax. That is a maximum contribution of $17,647 from your before tax wages. Which can be achieved with just a little help from your accumulated unused caps from previous years.

In short the scheme allows you to redirect $17,647 of your before tax wage into super leaving you $15,000 a year towards your deposit. If instead you had taken the $17,647 as wages you would have lost 39% in tax leaving only 10,764 or $207 per week in take home pay. This arrangement will increase the amount you can save by nearly 50%.

Note if you have already made some voluntary contributions to super these may also qualify to be withdrawn to buy a home

At the end of two years you have a $30,000 deposit, plus a bit of earnings on it and hopefully you have saved a little bit. Let’s say you have $35,000 to use as a deposit plus savings for the stamp duty which should be minimal on your first home.

How to Buy a House with $35,000

A lot depends on the price of houses in the area you want to buy in but there are also incentives for families. Here is a guide to how much you will have available to spend, without having to pay lenders mortgage insurance, depending on the dynamics of your household.

It is important to note that there are two tests you need to pass with the bank and it doesn’t matter how well you do on one, you still have to pass the other.

- The first test is having enough deposit. This is achieved without mortgage insurance by either having saved 20% of the house price or qualifying for the government deposit guarantee discussed further on.

- The second test is your ability to meet the repayments, which is determined by how much you borrow in relation to how much you earn and your family dynamics. Here is a link to a useful calculator https://www.westpac.com.au/personal-banking/home-loans/calculator/mortgage-calculator/maximum-borrowing-calculator

The following addresses your family dynamics and what your $35,000 deposit will allow you to buy. You still need to run through the calculator in 2 above to make sure the bank will lend you that much. That is the catch with low deposit borrowings. If you only have 5% deposit then you have to pay off a whopping 95% of the purchase price where as a 20% deposit for the same house will result in a much smaller loan and smaller repayments because you are only paying back 80% of the purchase price.

So here is the plan based on your family dynamics – continue reading even if you are single there is a plan for you too:

- Sole Parent – The government will guarantee your deposit when you have as little as 2% but you still have to be able to afford to pay off the 98%. If you have $35,000 plus stamp duty as a deposit then you can borrow $1.715 mil but of course you probably can’t afford the repayments on such a large loan. The point here is its not the deposit it is about using this calculator https://www.westpac.com.au/personal-banking/home-loans/calculator/mortgage-calculator/maximum-borrowing-calculator to see what the banks will lend you. But if you have a good income you should have no problem getting a modest home in most parts of Australia.

- Couple with Children – The government will guarantee your deposit when you have as little as 5% deposit. The ability to repay test should be a lot easier to pass with two incomes and with two incomes over the last 2 years you may have managed to save two lots of $35,000. But let’s say you haven’t had two incomes for the last two years because one parent has been at home with children. Now they are return to work your savings are diminished but you have stuck with the super savings scheme for the working spouse so have just $35,000. This will allow you from a deposit point of view to borrow $665,000 allowing you to purchase a house for $700,000 assuming now you are back on 2 incomes you can afford the repayments on $665,000. Might not get you inner Sydney but it should get you into most areas.

- Couple with no Children – Forget the government guarantee on your deposit unless you move to South Australia, see more information below. You will need the full 20% in order to avoid lenders mortgage insurance. But if you have no children then both of you can participate in the super savings scheme so you will have $70,000 deposit which will allow you to borrow $280,000 which, on two incomes you should have no problem repaying. The trouble is this only gives you $350,000 to spend on a property so possible, but very limiting. Just one extra year of saving will give you a $105,000 deposit allowing you to buy a property worth $525,000 which is getting much closer to the mark.

- Single Person no Children – No government guarantee unless you move to South Australia, see more information below. So you will need the full 20% deposit just like above but with only one income to pay off the loan so ability to repay is also an issue. Use this calculator https://www.westpac.com.au/personal-banking/home-loans/calculator/mortgage-calculator/maximum-borrowing-calculator to see what the banks will lend you. While the $35,000 from the super saver scheme will certainly help, you are going to have to save another $300 per week out of your take home pay over those two years as well and even then only be able to spend around $350,000. You may need more time, a second job, move to South Australia where you will only need a 3% deposit, a frugal lifestyle for 2 years, move back with parents or decentralize but it will be worth it. Two years is not that much time in your whole life-time to get to the next level of wealth creation. It is that first house that is the hurdle, after that you have a great source of cheap borrowings for further investment.

If you do make some extra savings over and above the contributions to super consider living off them at the start of the third financial year of saving so that you can contribute all of your wages into super for a few months to get the tax benefits on another $15,000. The maximum is $50,000.

Just a technicality here for full disclosure. If when you withdraw the funds from super and do not use them in the appropriate way they go in your tax return as income but with a 30% tax offset. From 1st July 2024 the marginal tax rate for income between $45,000 and $200,000 is only 30% so this works perfectly with your time line. As long as you play the game right there should be no tax, just Medicare Levy on taking the money out even if you decide not to buy a house. Make sure you have private health insurance if this is going to take your income as a single person with no children beyond $90,000 or at couple combined beyond $180,000.

You must apply for release of the funds before signing a contract GN 2018/1.

Once your savings have been released, you have up to 12 months (or other period allowed) from the date you requested the release of FHSS amounts to sign a contract to purchase or construct a home.

The contract you enter into has to be for a residential premises located in Australia. It cannot be any of the following types of property:

- any premises not capable of being occupied as a residence

- a houseboat

- a motor home

- vacant land except house and land packages.

Note: If you purchase vacant land to build a home on, it is the contract to construct your home that must be entered into to meet the FHSS scheme requirements. The contract to construct that home must be entered into within 12 months (or other period allowed) from the date you requested a release. In this situation you must not have purchased the vacant land before applying for a FHSS determination.

How the Federal Government Guarantee of Your Deposit Works

The places for this are limited and released each year so it is a step of faith to save through super with this in mind but as you can always choose to withdraw those savings from super and pay the top up tax, it is no longer a case of buy a home or your savings are lost until you retire.

If you qualify for the government guarantee the bank treats you as having a full 20% deposit for that side of the two tests. They don’t charge you mortgage insurance on the shortfall because the government is the mortgage insurer. You need to have a child to qualify for this scheme and you still need to repay the full amount you are borrowing. To be clear, the government are only guaranteeing your deposit not paying for it. So if the government offer a 15% guarantee because you only have 5% deposit you still have to make repayments on 95% of the purchase price, test number two.

This guarantee also has an income cap of $125,000 for singles and $200,000 for couples but this is as per your notice of assessment, taxable income. This means that those contributions to super will not be counted as your income for this test. A win win!

You also need to be an Australian resident over 18 intending to live in the property. There is also a cap on how much the property can cost depending on the location. Go to this page and put in your area’s post code https://www.nhfic.gov.au/what-we-do/property-price-caps/

For more information https://www.nhfic.gov.au/what-we-do/support-to-buy-a-home/first-home-guarantee/

How the State Government Guarantee of your Deposit Works in South Australia

How clever is South Australia! This is the perfect scheme to attract skilled labour to the state. To qualify for this government guarantee you have to have an education level of certificate III or higher and live in or move to South Australia.

The lender is a South Australian government organization and they only require a 3% deposit providing you can afford to pay off a loan for the other 97%. Houses are generally cheaper in South Australia as it is.

For more information https://www.homestart.com.au/home-loans/low-deposit-loans/graduate-loan

Don’t give up it can be done!